One of the most widespread misconceptions in SaaS development is the assumption that building a multi-vendor platform is closer to building a standard subscription product. Obviously, it is not. Marketplace payments do not equal SaaS subscription checkouts.

When you process payments for third parties, you enter a labyrinth of regulatory compliance, vendor payouts, chargeback liabilities, and complex taxation. Choosing the wrong payment provider will not just make the payment process less convenient and more suspicious for your users but also can trigger IRS audits, freeze your funds, and fundamentally break your unit economics.

For big companies and SMEs, selecting the right Stripe Connect marketplace architecture or evaluating alternatives like Paddle and PayPal is the main technical decision you will make.

In this article, you will find an expert breakdown of marketplace payment systems, taxes, and architectural tradeoffs for 2026.

SaaS Payments vs Marketplace Payments

To better understand the complexity of these terms, it is worth explaining the flow of funds via basic examples.

Single Merchant (Standard SaaS):

A User pays $50. The payment processor takes up to a ~2.9% fee. The remaining ~$48.55 goes directly into your corporate bank account. The recognized revenue is taxed.

Multi-Seller (Marketplace):

A User pays $100 for a service provided by a vendor on your platform. It is not allowed to simply take the $100 and wire $80 to the vendor after. If you do so, such action will be registered as an unlicensed money transmission. Thus, a special licensed system integration is required that captures the funds, splits the payment, routes your 20% commission to your account, and sends the 80% directly to the vendor’s account, tracking tax liabilities throughout the whole process.

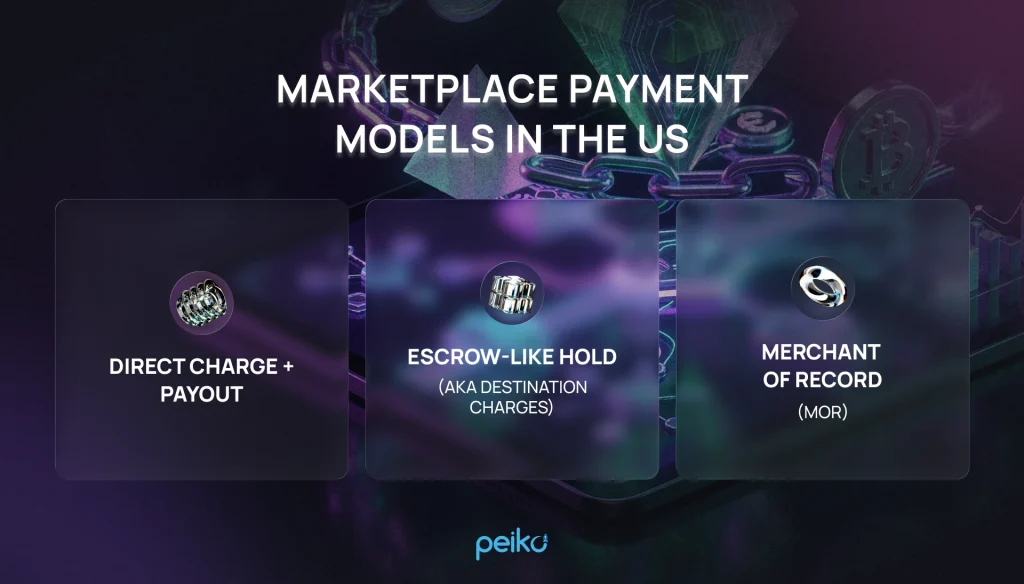

Marketplace Payment Models in the US

In the US, platforms typically process their payments within one of the following financial models:

Direct Charge + Payout: Within this model, the platform facilitates the whole payment. The buyer’s receipt shows the vendor’s name. The payment processor splits the funds instantly.

Escrow-like Hold (aka Destination Charges): This model covers the capture of the funds by the platform and holding them. The hold is usually provided by the payment processor’s ledger. Then, when the condition is met (=service was delivered), the payout is triggered. This protects the platform from chargebacks on undelivered goods.

Merchant of Record (MoR): Here, the platform technically buys the goods (services) from the vendor and immediately resells them to the buyer. This is the fundamental difference from a payment processor: with an MoR, the legal transaction is between the customer and the platform, while in Stripe-style processing the seller remains legally responsible for chargebacks, sales tax, and compliance.

Stripe Connect for Marketplaces (The US Default)

When mentioning multi-vendor platforms in the US, a Stripe Connect marketplace is the undisputed industry standard. This service was initially aimed at handling complex routing, KYC, and US tax compliance, which is also a core part of the broader paddle vs stripe discussion for teams comparing marketplace infrastructure.

Stripe Connect offers three main integration types:

- Standard (common integration): Vendors connect their own Stripe accounts that were set up and configured in advance. The vendor is responsible for chargebacks. In the context of development, this option is an easy way to build swiftly, but it provides the platform very little control over the UX

- Express: A popular option for most US startups with a more complex and hybrid approach. Stripe provides the onboarding UI and tax reporting, which saves more time for the management team. However, the platform controls the User experience and the flow of funds.

- Custom: Full white-label control via building the entire onboarding UI via API. The platform is fully responsible for managing the user experience, but Stripe still handles the backend compliance.

Key Features of the Stripe Connect Integration:

- Onboarding & KYC: The integration verifies vendor identities (SSN, EIN, ID uploads) to comply with US anti-money laundering (AML) laws.

- Scheduled Payouts: Stripe Connect allows configuring daily, weekly, or manual payouts.

- Refunds & Chargebacks Processing: Defines the system-level permissions for working with chargebacks, either through the platform account or the vendor’s connected account.

- Webhook Reliability: Stripe’s event-driven webhooks have a wide range of functionality, allowing the backend to react instantly to payment success, dispute creation, or vendor verification failures. Its API is often described as “poetry” and remains the gold standard for developer experience, giving teams extensive customization and control.

Paddle: Best Merchant of Record for SaaS, Limited for Marketplaces

Paddle is an incredible tool for traditional B2B SaaS companies running a subscription business because it acts as a Merchant of Record (MoR). It is the legal seller and handles global tax compliance by calculating, collecting, filing, and remitting sales tax and VAT on the seller’s behalf.

- The MoR Advantage: With Paddle, there is no need to worry about registering for sales tax in 50 US states or VAT in Europe, which makes it more hands off for teams selling globally while staying aligned with local laws, including European Union VAT rules. Paddle integration takes responsibility for the legal liability of the transaction.

Paddle uses hosted checkout flows, which simplify compliance but reduce complete control and customization options compared with Stripe.

Paddle’s faster integration suits SaaS companies that prioritize speed to market over maximum control.

- The Marketplace Limitation: Paddle’s main aim is not a multi-vendor payout engine. Based on the previous example, they do not have native functionality to split a $100 payment, run KYC on a third-party vendor, and route $80 to that vendor’s bank account. If the platform uses Paddle, the business generally has to handle vendor payouts manually (or via a separate API like Wise), which involves additional compliance risks and operational overhead.

Paddle’s typical fee is 5% + $0.50 per transaction, bundling payment processing, fraud protection, and tax features.

PayPal for Marketplaces (Pros & Cons, and When It Works)

For the marketplace platforms, PayPal offers a PayPal Braintree / PayPal for Marketplaces service.

- US Compliance and User Trust: PayPal is a well-known brand, and using it at checkout boosts conversion rates for websites that interact with customers, but some providers also accept payments through broader methods such as bank transfers via a payment gateway setup.

- UX Tradeoffs: Compared to Stripe‘s API, the integration and developer experience are frequently less sophisticated.

- Limitations for Split Payouts: PayPal’s risk models are strict, even though it allows multi-party payments. If PayPal’s algorithm notices a spike in volume or disputes, it frequently freezes marketplace funds for up to 180 days, which can destroy a startup’s vendor trust.

US Sales Tax & Compliance Basics

The business owners often neglect compliance at the initial steps of the marketplace development until they receive fiscal or legal consequences. To minimize these risks, you need to architect for the following:

- 1099-K Reporting: The IRS requires marketplaces to report gross payment volume for US vendors meeting certain thresholds. If you use Stripe Connect, Stripe will generate and file these forms automatically. If you build a custom payout engine, you must build the 1099-K reporting infrastructure.

- KYC (Know Your Customer): You cannot pay out funds without verifying who is receiving them. Doing so risks facilitating money laundering or violating OFAC sanctions.

- Marketplace Facilitator Concept: Over 40 US states have enacted laws stating that if a marketplace facilitates a sale, the marketplace (not the individual vendor) is responsible for calculating, collecting, and remitting state sales tax. With Stripe-style processing, the seller still bears tax liability for calculating, collecting, and remitting sales tax in every jurisdiction where customers are located, and must stay compliant with tax authorities and local laws.

- Terms of Service + Dispute Policy: Your Terms of Service must legally establish your role. Are you an agent of the seller? A neutral venue? This defines your liability when a transaction goes wrong.

Payment Gateway Architecture Considerations

Your marketplace architecture must treat financial data with an extreme level of care.

You are not just building a web app; you are building a financial ledger.

- Webhook Idempotency: Financial webhooks will occasionally be sent twice by providers like Stripe due to network retries. Your backend must process webhooks idempotently (using a unique event ID) so you do not accidentally credit a vendor twice for the same transaction.

- Double-Entry Ledger & Audit Trail: Your marketplace database design must include an immutable ledger. Every financial event (Payment Authorized, Payment Captured, Platform Fee Deducted, Payout Initiated, Payout Failed) must be recorded as a discrete, timestamped row. Never simply UPDATE a user’s balance column.

- Reconciliation: Build internal admin tools that reconcile your database’s understanding of vendor balances with Stripe’s actual API balances on a daily cron job.

- Security: API keys and webhook signing secrets must be strictly managed via environment variables and secrets managers (like AWS Secrets Manager), never hardcoded.

How Payments Affect Marketplace App Development Cost

Integrating a robust payment and payout engine significantly impacts your marketplace app development cost, and that matters in a paddle vs analysis for SaaS payments infrastructure.

- Scope Creep: Implementing checkout is a swift solution. Instead, it is worth taking into account that implementing the lifecycle of a marketplace payment (authorization, holding funds, splitting fees, vendor KYC, handling failed payouts, processing chargebacks, and generating tax documents) takes weeks or months, depending on the individual requests. In paddle vs Stripe decisions, Stripe’s base fee is typically 2.9% + 30¢ per transaction, but the total cost can rise due to add ons, tax compliance work, fraud prevention tooling, and other operational overhead, which adds additional cost beyond core billing.

- Admin Tools: Building internal dashboards could cause significant budget spending. When a vendor emails support asking, “Why wasn’t I paid?” the platform support team needs an interface to see the source of the case (for example, the KYC verification failed, or the bank rejected the ACH transfer).

- Reporting: Building custom CSV exports for your accounting team to reconcile platform revenue vs. vendor payouts adds development overhead. With Stripe Billing, teams with complex subscription management or advanced billing workflows may also need an additional tool, while other features increase the total cost of ownership.

What to Choose: Decision Matrix

Below you can see a decision matrix to guide your choice between paddle and stripe:

Summary: Final verdict: for most US-based multi-vendor platforms, the decision in Paddle vs Stripe comes down to convenience vs Stripe flexibility, and Stripe Connect is often the stronger fit for payout automation, developer experience, and tax compliance. Some teams choose Stripe for complete control, especially when they need unique billing structures, maximum control, and have dedicated finance resources to manage the operational burden.

Common Mistakes: the US Marketplaces

- Leaving Payouts “For Later”: A payout architecture cannot be added at the last minute. On the first day, the entity relationships between users, orders, and financial ledgers need to be designed.

- No Chargeback Strategy: Who is responsible for paying if a buyer contests a $500 charge and the bank returns the money? Your platform just lost $500 if the vendor has already been paid. Automated clawbacks or delayed payouts require coding.

- Weak Admin Tools: While engineering teams enjoy creating buyer user interfaces, they detest creating admin panels. Your customer service operations will fail if you don’t have a detailed financial dashboard.

- Misunderstanding MoR: Teams comparing paddle and stripe often miss the split in responsibilities: with Paddle, the MoR handles more of the tax and compliance burden, while with standard Stripe you still own tax setup, refunds, and much of the billing lifecycle unless you add more tools.

Conclusion

Building a multi-vendor platform in the US requires you to act like a fintech company just as much as a software company. The complexities of compliance, taxation, and asynchronous event architecture mean that standard web development often fails to deliver a product that survives contact with the real world.

Before setting up a single action of payment logic, ensure you have validated your core platform assumptions. Read our comprehensive guide on how to build a marketplace app to understand the foundational product steps.

If you are ready to execute your vision and need an expert team that understands the deep technical requirements of a payment service provider ecosystem, it is time to hire SaaS developers who specialize in high-stakes marketplace app development. Let’s build a platform that scales securely and compliantly. Contact us to deliver a high-quality product that fits the market demand and assists you in reaching the top of the market!

No comments yet. Be the first to comment!