Even the most complex passwords can be stolen, and databases remain vulnerable to breaches. DID verification offers to turn credentials from copyable data into verifiable, tamper-evident proofs every stakeholder can trust across borders and systems.

In this guide, we explore what blockchain digital identity is and why traditional models keep failing. You’ll discover the concrete security gains, see where real industries are deploying it today, and learn about the risks you should address. We’ll also look ahead at what’s coming next!

If safeguarding customer data and streamlining compliance are your goals, keep reading! By the end, you’ll know whether blockchain digital identity fits your strategy, how your business can benefit, and how to choose the right path forward. Let’s dive in.

What is a decentralised digital identity?

Instead of scattering copies of your personal data across dozens of databases, you hold cryptographically signed and proven credentials in a secure wallet on your phone or laptop. This is the essence of the blockchain digital ID. When a bank, employer or website needs to verify your personal data, you then share proof, and they can instantly validate it against a tamper-evident record on a blockchain.

Below is the simple illustration for the whole process:

- You (the holder) keep your identity assets — name, age, employee status, certifications, etc. (any kind of data really) — in a digital wallet.

- Trusted issuers (universities, banks, governments) create verifiable credentials and sign them with corresponding private keys.

- Verifiers (apps, merchants, services) check those credentials’ signatures against decentralised identifiers (DIDs) anchored on a blockchain to confirm uniqueness and immutability.

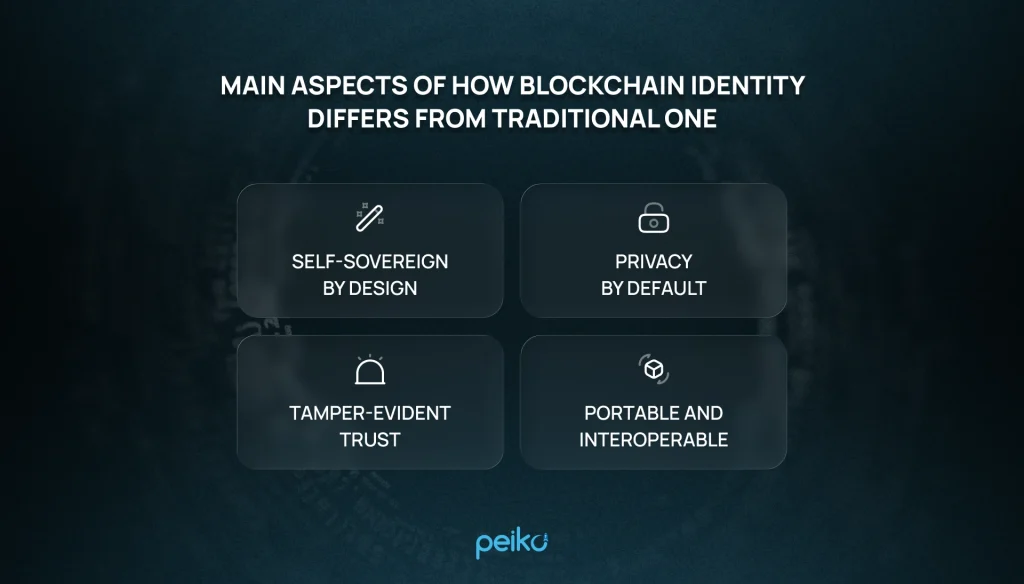

A few key principles make this different from today’s login-based world:

- Self-sovereign by design. You control your identifiers and credentials. No single provider can lock you in, track you across sites, or take control over your account.

- Privacy by default. Share the minimum—“over 18,” “KYC (know your customer) checked,” “licensed nurse”—using selective disclosure and, where supported, zero-knowledge proofs. Your full date of birth or certificate number stays with you.

- Tamper-evident trust. The blockchain ID is a public trust layer for keys, schemas, and revocation lists. Your data is kept off-chain with you, while the blockchain shows if anything was changed.

- Portable and interoperable. The same credential can unlock services across borders and platforms, reducing repetitive onboarding and compliance friction.

A quick example: a university issues you a digital diploma. Years later, a recruiter scans a QR code from your wallet. In seconds, their system confirms the credential was issued by that university, hasn’t been altered, and hasn’t been revoked. Everything happens in seconds instead of wasting hours calling registrars or storing extra copies of your records.

Why does this drastically matter for security? Eliminating centralised data silos shrinks the attack surface. Cryptographic verification delivers security-wise, while proof-based sharing limits the impact if one service is compromised. Users can feel the innovation through faster checkouts and shorter onboarding. For businesses, it’s trusted data, significantly decreased number of false positives, and simpler compliance.

In short, the advanced DID management turns identity from a pile of copyable records into portable, verifiable proofs. This means a solid foundation for safer, smarter access in every industry.

Why traditional digital identity systems fail

Traditional digital identity was built for a web of passwords, not for a world where data moves across clouds, apps, partners, and countries. Most systems copy your personal details into many separate databases. That makes onboarding repetitive, raises costs, and turns every database into a high-value target. When one of those platforms is breached, stolen logins and profiles spread across the internet through credential stuffing, phishing, and identity theft.

You hand in too much sensitive information to third-parties. In order to prove you’re eligible for a service, it is often mandatory to provide full birth dates, addresses, document scans, etc. After this stage, you are no longer in control of your personal data, hence you have no option but to trust each of the providers that your info is stored safely and deleted on time.

Ok, let’s add some fragile recovery flows (e.g. “What was your first pet’s name?”) and vendor lock-in—you’ll get a system that’s very easy to attack, hard to audit, and slow to use. More fraud, more friction, and rising compliance risk are direct results of such a system.

Traditional vs. blockchain-based digital identity at a glance

| Dimension | Traditional digital identity (accounts & databases) | Blockchain digital identity (verifiable credentials) |

| Who’s in control of sensitive data | Service provider. You get an account the provider can suspend | You! Credentials are stored in your digital wallet |

| Where sensitive data is stored | Copied into many provider databases | Kept with you. The blockchain holds only public keys and revocation markers |

| Trust & verification | “Because it’s in our database” | Public-Private Key Encryption – user’s side. Cryptographically proven security mechanisms under the hood. Verifiers check authenticity instantly. |

| Risk of mass breach | High — single database stores all the information -> cyber incidents can compromise everything | No central server to attack.Risk is significantly lower — you get lots of best security practices “out of the box” + can develop custom measures on top. |

| Data shared per transaction | Often excessive (full profile) | Minimal, purpose-bound proofs ( “over 18” without your exact birth date) |

| Resistance to phishing & stolen passwords | Weak — passwords and one-time codes can be compromised by an adversary | Strong — proofs are device-bound and non-reusable. However, you are the only person responsible for storing your private keys (passwords in this context) as no one can recover them for you. |

| Portability across apps | Low — repeat forms and checks per service | High — reuse the same credential anywhere it’s accepted |

| Onboarding effort & cost | Manual checks, slow document review, duplicate KYC across vendors | Issue once from a trusted source. Reuse cuts time and operational cost |

| Revocation & updates | Inconsistent—each provider must update its copy | Unified — issuers can publish status so verifiers see changes immediately |

| Compliance & auditability | Hard—data sprawl, unclear consent trails | Easier — clear issuance, consented sharing, and machine-verifiable logs |

| Vendor lock-in | High—identities tied to a platform’s account system | Low — standards-based wallets. Credentials work across providers |

| Account recovery | Security questions, email resets | Recovery plans and delegated guardians with no shared secrets exposed |

Traditional systems scatter and overexpose your identity. DID replaces copies with portable proofs, reducing breaches while speeding up onboarding and access.

How identity verification works on a blockchain

Three actors comprise the blockchain and identity management: issuers (who vouch for something about you), holders (you), and verifiers (the app or service that needs to check a claim). The blockchain anchors public keys, schemas, and status. Anyone anytime can verify authenticity without constantly calling the issuer.

At the center is your identity wallet—an app on your phone or laptop that stores your keys and your credentials (“over 18,” “employee at X,” “certified nurse”). When a bank or website asks for proof, your wallet creates a one-time, tamper-evident presentation. The verifier checks the cryptographic signatures/hashes against information anchored on a blockchain, confirms the credential hasn’t been revoked and grants access. The whole process is a matter of several seconds.

Key building blocks you’ll encounter:

- Decentralised identifiers: your and the issuer’s public keys, linked to a blockchain for integrity.

- Verifiable credentials: cryptographically signed evidence that you can store and reuse across services.

- Status & revocation registries: machine-readable lists issuers update so verifiers spot expired or revoked credentials.

- Selective disclosure & zero-knowledge proofs: share only what’s needed (e.g. has the right to vote in X country).

Issuance is straightforward and easy-to-understand to a novice. A trusted organization verifies you once (checks a passport) and issues a signed credential to your wallet. From that point, you’re able to reuse the credential anywhere it’s accepted. Because the issuer’s public key and the credential schema are stored on a blockchain, anyone can validate the signature and integrity independently.

In practice, Verification process looks like the following:

- You scan a QR code or approve a prompt in your wallet.

- An executable piece of code on a blockchain responds with a request to sign a message using your wallet.

- Your wallet assembles the minimal proof requested (the message), and signs it.

- Transaction is being included to the block and then verified on the blockchain

- The verifier (organisation) checks signatures, issuer trust, and revocation status via the blockchain anchors and then decides.

Security operates at multiple layers. Device binding and secure hardware protect your keys. One-time presentations stop replay attacks. Consent prompts and audit trails ensure sharing is transparent and traceable.

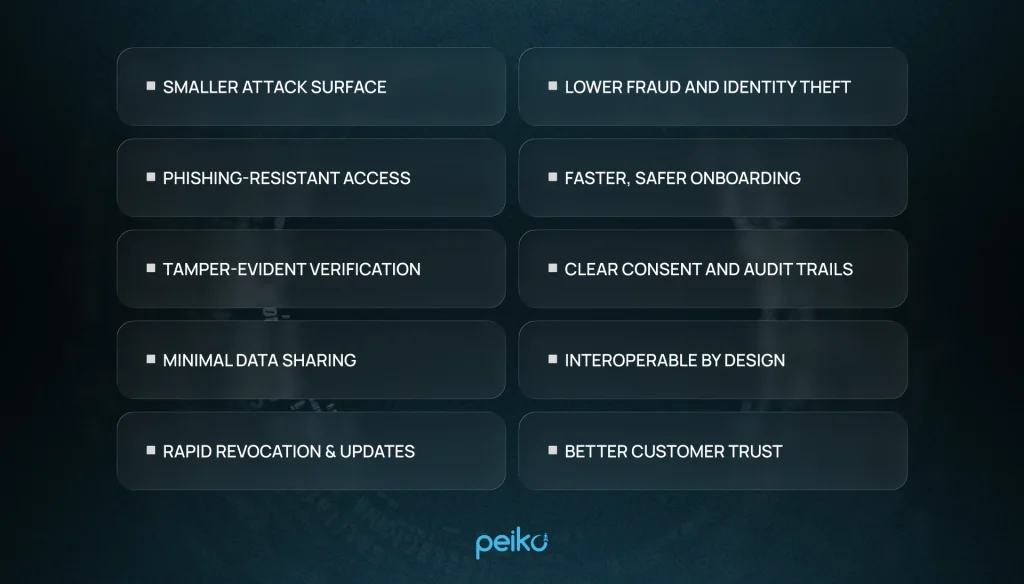

Key benefits of blockchain digital identity for data security

Organizations and users disclose only the minimum required attributes. Verification occurs via tamper-evident signatures rather than database lookups. We get a smaller attack surface, higher assurance, and faster, safer access across platforms and jurisdictions.

Tangible benefits for users and businesses

Users get faster, safer experiences with greater control over their data, while businesses cut costs, reduce fraud, and streamline compliance. The net effect is higher trust, better retention, and measurable ROI. Here’s how identity on blockchain translates into notable gains:

- Smaller attack surface: Your details aren’t copied into dozens of databases. Most sensitive data stays in your wallet.

- Phishing-resistant access: No reusable passwords to steal. Logins rely on device-bound keys and one-time proofs that can’t be replayed.

- Tamper-evident verification: Claims (like “over 18” or “employee at X”) are digitally signed by trusted issuers and checked automatically. There are no manual lookups or PDFs.

- Minimal data sharing: Prove facts without exposing raw data (confirm age without sharing your birth date). Less exposure, and less to lose in a breach.

- Rapid revocation & updates: If a credential expires or is revoked, verifiers see it instantly. You can cut off access quickly when roles change or risk emerges.

- Lower fraud and identity theft: Credentials are cryptographically bound to issuers and your device, making the creation of fake accounts and synthetic identities much more difficult.

- Faster, safer onboarding: Verify once from a trusted source; reuse everywhere it’s accepted. Fewer document uploads, manual checks, and errors.

- Clear consent and audit trails: Every share is explicit and logged, helping with privacy regulations and internal audits without sprawling data copies.

- Interoperable by design: Open standards mean the same credential works across apps, partners, and countries, reducing risky custom integrations.

- Better customer trust: Private blockchain by default (share the minimum, only when needed) builds confidence without adding friction.

DIDs shrink breach risk while speeding up verification. You move from storing and defending piles of personal data to validating precise, tamper-evident proofs—stronger security with less friction.

Industries leveraging blockchain identity verification

Here’s a quick tour of who’s using DIDs verification right now (2024–2025), what they shipped, and why it matters.

Government & national ID — South Korea’s mobile ID

Example: Korea’s mobile Resident Registration Card (mID) rollout

South Korea completed a nationwide rollout of digital IDs that citizens can add to their smartphones. The program builds on earlier drivers-license wallets and is explicitly described by Korea’s state mint (KOMSCO) as using blockchain-based decentralized ID to anchor issuance logs and protect integrity.

Banks, airports, and hospitals accept the mID with the same legal standing as the physical card, streamlining KYC and public-service access.

Travel & aviation — Digital Travel Credential at scale

Example: Aruba + SITA + Indicio Digital Travel Credential (DTC)

In 2024–2025 they documented broader airline integrations and operational results.

Education — EU universities issuing blockchain-anchored diplomas

Example: EBSI-VECTOR pilots (EU)

Across Europe, universities are issuing verifiable diplomas that graduates store in an ID wallet and present to employers as a proof the employer can instantly verify against the European Blockchain Services Infrastructure (EBSI).

Danish universities piloted issuance at scale, and the University of Lille outlined 2024–2025 cohorts using blockchain-anchored credentials—cutting manual checks and fraud.

Banking & fintech — Verifiable LEIs (vLEI) go on-chain

Example: GLEIF’s vLEI + Chainlink (2025)In the blockchain fintech field, Global Legal Entity Identifier Foundation’s (GLEIF) verifiable Legal Entity Identifier (LEI) standard (ISO 17442-3:2024) turns the LEI into a cryptographically signed credential that proves an organization’s identity (and even a person’s role within it).

In June 2025, GLEIF and Chainlink published a model for bringing vLEIs on-chain, so smart contracts can automatically check a company’s identity before executing finance workflows—useful for payments compliance and counter-party risk.

Luxury & retail — Product identity (Digital Product Passports)

Example: Aura Blockchain Consortium (LVMH, Mercedez-Benz, Prada Group, Cartier/Richemont, OTB)

Luxury brands are assigning each product a blockchain-backed digital identity that customers can scan to verify authenticity, provenance, and service history.

")

Aura passed 50+ million products recorded by late 2024 and continues expanding as EU Digital Product Passport rules approach—reducing counterfeits while enabling circular services like repair and resale. From national IDs and airport corridors to diplomas, bank onboarding, and even handbags, the distributed ledger networks pattern repeats: database lookups replaced with portable credentials and on-chain trust anchors. That yields faster verification, less data exposure, and stronger fraud resistance.

Challenges and risks of decentralised identities

Here’s a cleaner cut. DIDs can greatly reduce data sprawl and fraud. But it also relocates risk—from central databases to keys, wallets, governance, and ecosystem rules.

Most problems are socio-technical: technology, regulation, and user behavior intersect. Below, we present both the risks (what can go wrong) and the challenges (what’s hard to execute well).

Risks (negative outcomes if things go wrong)

Even excellent systems can fail if a phone gets hacked, keys are eventually lost, or bad data slips through. This list shows the main ways things can break and what the damage could be—so you know what to watch for and plan around.

- Wallet or device compromise: Malware or stolen phones can approve fraudulent proofs.

- Key loss without recovery: Lost keys or hardware = lost access to credentials.

- Oversharing via malicious requests: Users may click “share” on excessive attributes.

- Issuer mis-issuance or fraud: Perfect signatures on false claims; unclear liability.

- Stale or revoked credentials accepted: Outages or poor status checks lead to bad decisions.

- Privacy leakage/correlation: Reused identifiers or metadata can reveal patterns.

- On-chain immutability mistakes: Publishing personal data or sensitive metadata is permanent.

- Third-party dependency outages: Trust registries, status services, or layer 2 networks go down.

- Regulatory penalties: Misaligned data handling, consent, or record-keeping triggers fines.

- Vendor lock-in: “Open” solutions that quietly depend on proprietary wallets.

Challenges (hard problems to design and operate)

Building blockchain identity that’s safe, private, and easy to use in long-term while also at scale isn’t trivial at all. These are the tough design and operational hurdles teams must solve to make it work in the real world.

- Safe and usable recovery: Guardians, backups, or multi-device setups without new attack paths.

- Strong wallet baselines: Secure hardware, attestation, and phishing-resistant consent UX.

- Interoperability: Aligning identifiers, credential formats, and trust lists across vendors and countries.

- Governance and role control: Who may issue which claims, how to audit them, how to remove bad issuers.

- Revocation at scale with privacy: Fast status checks that don’t enable tracking.

- User experience & inclusion: Clear prompts, offline options, and support for people without high-end devices.

- Scalability & cost: High-volume issuance/verification without latency spikes or fee shocks.

- Legacy integration: Mapping proofs into existing IAM, CRM, and compliance workflows.

- Data-minimization by default: Enforcing “prove just enough,” not “upload the document anyway.”

- Cross-border legal alignment: Reconciling sector rules and national laws so credentials are accepted everywhere.

- Incident response & auditing: Privacy-preserving logs that still support forensics and proof of consent.

Blockchain identity is a complete system. Embracing it, you become aware how to manage the risks with strong wallets, recovery, revocation, and privacy patterns, tackle the challenges with clear governance, interoperable standards, thoughtful UX, and tight integration with your existing controls.

The future of blockchain digital identity (2025-2028)

Authentication is going passwordless. By late 2024, 15+ billion online accounts could leverage passkeys, and adoption is accelerating: Amazon reports 175M customers have enabled passkeys (with 6× faster sign-ins), Google logged 1B+ passkey authentications across 400M accounts within a year, and Microsoft now sees ~98% sign-in success with passkeys and nearly a million new passkeys registered daily.

This wallet-native authentication pairs naturally with verifiable credentials to deliver “who you are” plus “you’re here now” in a single, phishing-resistant flow.

The threat landscape makes the shift urgent. The U.S. FTC (Federal Trade Commission) reports consumers lost $12.5B to fraud in 2024 (+25% year-over-year), while enterprise identity pipelines are seeing more hostile noise—1 in 20 verification attempts was fraudulent in 2024, and 60%+ of organizations observed a rise in AI-driven attacks.

That’s why the future of decentralised identity isn’t just about wallets and credentials. It’s AI-assisted fraud defense, phishing-proof authentication, and privacy-preserving verification working together.

Below are the seven most prominent future-facing angles. Learn what each of them means, what value it brings, near-term implications, plus practical KPIs (key performance indicators).

1) Enterprise-grade credentials (KYC/KYB & roles)

Reusable, issuer-signed credentials for customers (KYC), businesses (KYB – know your business), and workforce roles/permissions. “Verified Person,” “Verified Company,” and “Approved Signer” proofs that can be presented across banks, fintechs, marketplaces, and SaaS tools.

Why it matters

- Cuts repeat onboarding: verify once, re-use many times.

- Hardens trust at the edge (marketplaces, partner APIs—application programming interfaces).

- Auditable by design—issuers, schemas, and status checks are machine-readable.

Near-term implications

- Onboarding drops from days to minutes for known users.

- B2B sales cycles shorten as counterparties can verify company status and authority in-flow.

- Access control shifts to signed role credentials (“Finance-Approver L2”) instead of ad-hoc admin lists.

KPIs

Onboarding time ↓, abandonment rate ↓, manual reviews ↓, fraud chargebacks ↓, audit exceptions ↓.

2) Key recovery that people can actually use

Use another device, ask trusted contacts, or combine key pieces to get back into blockchain identity solutions.

Why it matters

- Mitigation of the #1 blocker for non-custodial identity—the fear of lockout.

- Human-understandable, tamper-evident, and phish-resistant recovery.

Near-term implications

- No single point of failure. One lost device or breached service isn’t enough to take your assets. Your keys are split between your own hardware (phone or key) and secure pieces in the cloud.

- HR offboarding can revoke role keys while personal credentials persist with the individual.

- Recovery generates attestations to satisfy audits.

KPIs

Account-loss tickets ↓, successful self-recovery rate ↑, time-to-recover ↓, recovery-related fraud = ~0.

3) AI-assisted fraud defense

AI in blockchain helps check that people and documents are real during signup and use. It runs in your wallet/app, at the issuer, and at the service you’re using.

Why it matters:

- Helps block deepfakes and fake IDs without keeping your raw face data in one central place.

- Only asks for extra checks when the risk looks high.

What happens soon:

- If risk goes up, you might be asked for a quick “is it you” check that will confirm that the device you were using is truly yours. If not, nothing extra happens.

- When fraud is confirmed, the system learns and updates its rules.

- Keep data private: do the AI work on your device when possible; share only scores or proofs, not raw data.

KPIs

Synthetic identity rate ↓, false positives ↓, step-up rate vs. conversion (optimal), verified liveness success ↑.

4) Business models & ROI

Clear monetization and cost-savings levers for issuers, wallet providers, and relying parties.

Why it matters:

- Identity stops being just a “compliance cost” and starts driving revenue and savings.

- Buyers (procurement) need to see real, near-term savings and growth.

What happens soon:

- Pricing per check (“pay when a credential is verified”) vs. flat subscription. Stronger checks can cost more.

- Banks, telcos, and governments cut their KYC costs by issuing reusable credentials.

- Industry blockchain social networks (finance, mobility, creator tools) share trusted lists to speed things up.

- Real ROI (return on investment): fewer manual reviews, faster onboarding, higher conversion, less fraud loss.

KPIs

Cost per verified user ↓, lifetime value ↑ via faster activation, compliance OPEX (operating expenses) ↓, payback period (months).

5) Passkeys + identity wallets converge

Passkeys prove “it’s really you on this device right now.” Verifiable credentials prove “who you are.” Together they give passwordless, phishing-resistant login and let you share only the claims you need.

Why it matters:

- No more SMS codes or email links (both are easy to attack).

- One tap to sign in and share just enough info (“over 18,” “employee level 2”).

Near-term implications

- Simpler login—tap to authenticate and attach the needed claims to your session.

- For work accounts, SSO (single sign-on) plus role credentials, so people get only the access they need.

- Meets strong-auth rules without storing extra personal data.

KPIs

Password resets ↓, phishing incidents ↓, login success ↑, average auth time ↓.

6) On-chain business identity (vLEI and equivalents)

Cryptographically verifiable organization identities and authority credentials for signers usable by apps, APIs, and smart contracts.

Why it matters

- Automates counterparty checks in B2B workflows, trade finance, procurement, and DAOs (decentralized autonomous organizations).

- Reduces invoice fraud and impersonation, standardizing who can sign what.

Near-term implications

- Software can read who is allowed to sign what, and enforce limits automatically.

- Marketplaces and SaaS (software as a Service) verify a company once. Later, it’s just a status check.

- Works with existing trust frameworks and registries.

KPIs

Time-to-vendor-approval ↓, fraudulent vendor events ↓, rejected signatures ↓, automated approvals ↑.

7) Digital Product Passports & item identity

Verifiable digital “passports” bound to physical items—origin, materials, maintenance, ownership, repair— and discoverable by consumers and service networks.

Why it matters

- Helps stop counterfeits and supports resale, refurbishing, and recycling.

- Unlocks post-sale services (warranty, targeted recalls, parts matching) tied to the item itself.

What happens soon:

- Quick authenticity checks at resale. Loyalty can attach to the product.

- Service history makes warranty and second-hand sales smoother.

- Meets new rules for traceability and sustainability reporting.

KPIs

Counterfeit incidents ↓, resale conversion ↑, warranty claim time ↓, recovery/recycling rate ↑.

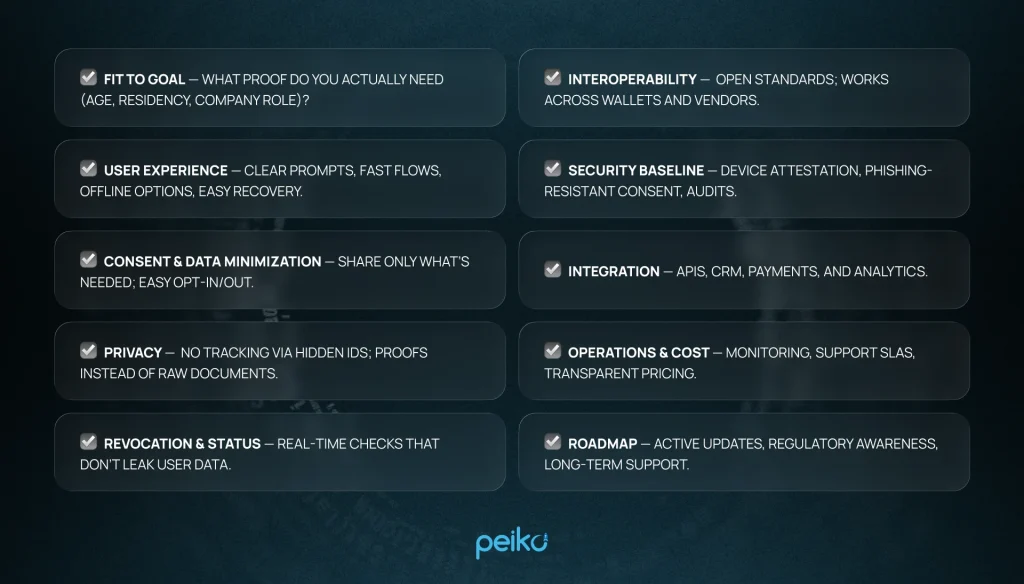

Choosing the right blockchain identity verification solution

How can your business benefit from DIDs if you don’t know how to choose the one that fits you?

Start with your industry and main goal. Are you reducing onboarding friction in fintech in 2025, proving age in gaming, or verifying merchants in a marketplace? Your use case decides the trust model, the strength of checks, and what “good UX” means.

Map your risk, compliance, and rollout needs. Check how the solution handles recovery, revocation, and privacy. Make sure it fits your stack, works with your wallet choice, and is affordable to run in the long term.

Practical checklist

Quick UX win — revisit the consent button:

Make it plain-language (“Share only date of birth? Yes/No”), show what’s being shared and for how long, and let users undo it later.

Peiko expertise in secure blockchain solutions

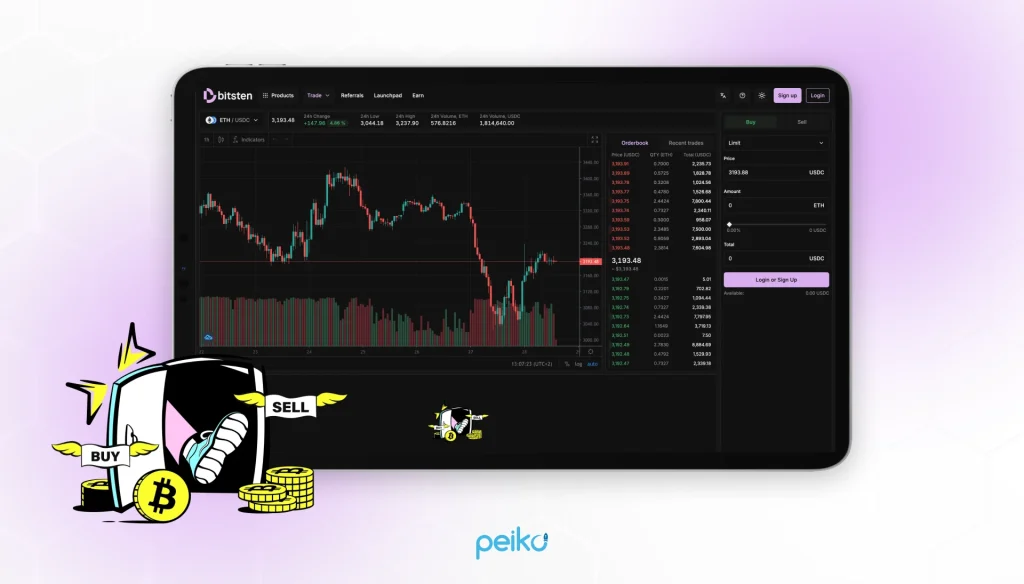

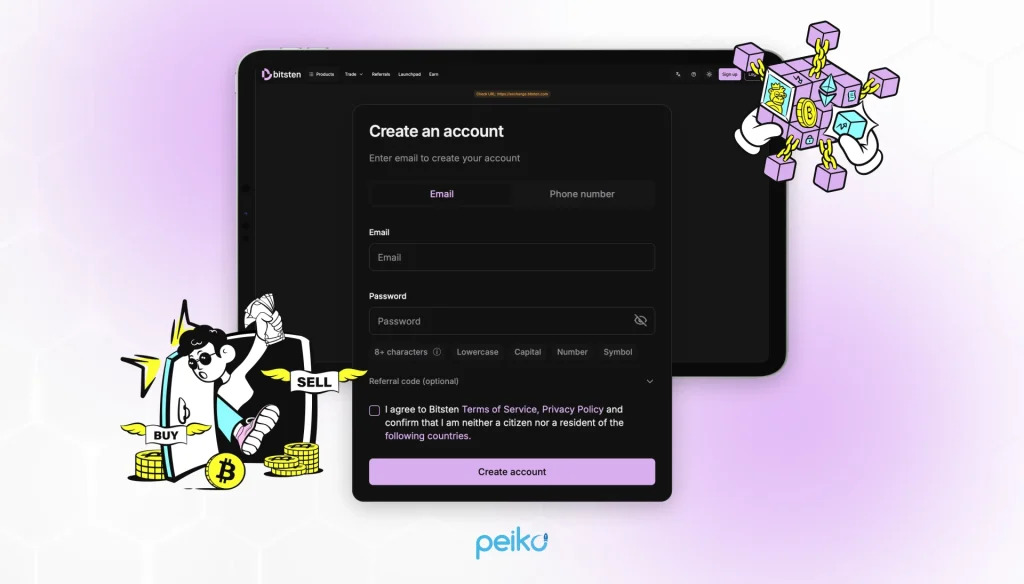

We build secure, scalable Web3 and software products end to end—from discovery and architecture to design, development, integrations, and launch. We focus on real-world reliability: strong security, clear UX, and smooth integrations with payments, analytics, and compliance tools.For instance, one of the recent clients needed a fast, budget-friendly way to launch a global crypto exchange ready to scale. They required real-time trading, multi-currency payments, and strong security, all delivered by a dedicated team on a tight timeline.

What we delivered. We shipped a high-performance, white-label exchange built on a Node.js microservice stack (Next.js + Nest.js), cloud-ready with Kubernetes and Azure. We handled BITSTEN development end to end and trained the client’s team for a smooth handover.Performance and operations. The system is engineered for roughly 10,000 transactions per second. Modular services make scaling straightforward and keep future feature work isolated, reducing risk during updates and spikes.

Integrations and safeguards. The platform streams live prices and instant execution, with liquidity routed through Huobi and B2C2. Assets are protected via Fireblocks and secure storage, while compliance runs through SumSub with DDoS protection. TradingView powers advanced charts, SendGrid handles notifications, and Stripe/PayPal enable multi-currency payments.

Outcome. Time-to-market dropped dramatically versus custom build. Security and compliance are baked in, user experience is fast and responsive, and the white-label base gives the client room to rebrand, extend, and expand globally.

Choosing a blockchain identity solution starts with your understanding of what you need, then drills into UX, privacy, security, and fit with your stack. Peiko brings the mix of product sense and engineering depth to turn that checklist into a working system. The Bitsten case shows we can ship fast, secure, and scalable platforms with the right integrations. If you’re ready to see real gains in onboarding speed, fraud reduction, and compliance—let’s build it!

Conclusion

Decentralised Digital Identity replaces copied personal data with portable, cryptographically verifiable proofs. Credentials live in a user wallet; issuers sign them; verifiers check signatures and revocation status on-chain. The result is a smaller attack surface, phishing-resistant access, faster onboarding, and clearer audit trails.

Over 2025–2028, expect passkeys and wallets to converge, reusable enterprise credentials to mature, AI-driven fraud defense to harden checks, and item identity to spread.

No comments yet. Be the first to comment!